Unauthorized reproduction or distribution is illegal and subject to criminal penalties.

Pharm Edaily enforces a zero-tolerance policy and will take strict action.

[Yu Jin-hee, Edaily Reporter] While the South Korean stock market has recently enjoyed a broad upward trend, the biotech sector on the 29th saw a sharp divide between “winners and losers.” Companies that proved their profitability through tangible clinical results and strategic licensing-out (L/O) deals successfully led the rebound. In contrast, those hit by the negative news of large-scale capital increases suffered steep declines. This market trend clearly indicates that investor sentiment is concentrating on companies providing “solid data” rather than vague expectations.

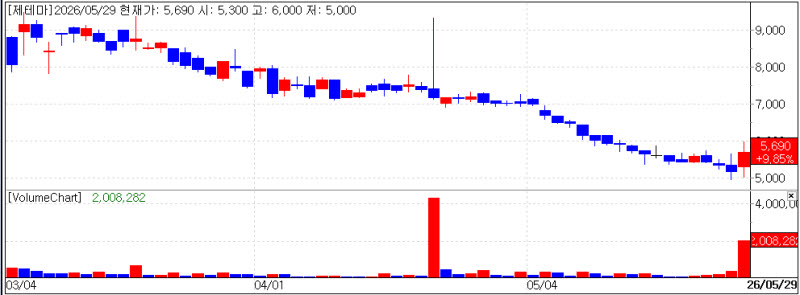

| | Recent stock price trend of Jetema. (Source: KG Zeroin MP DOCTOR) |

|

Jetema Ignites Global Growth Engine with Successful Phase 3 Results in China According to KG Zeroin MP Doctor, Jetema closed at 15,690 won on the 29th, up 9.85% from the previous day, bolstered by news of its successful botulinum toxin clinical trials in China. During the day, the stock surged over 10%, showcasing its dominance as a leader in the medical aesthetics market.

Jetema officially announced that the final Clinical Study Report (CSR) for its botulinum toxin product, ‘JTM201,’ has been approved for Phase 3 clinical trials in China. The study, involving 506 adult patients requiring improvement of moderate-to-severe glabellar lines, proved its non-inferiority to the original ‘Botox®.’ Four weeks after administration, the improvement rate in the JTM201 group was 77.8%, matching the 77.7% observed in the control group. Furthermore, over 60% of patients reported sustained effects at 16 weeks, demonstrating excellent long-term efficacy.

“This CSR approval proves that the consistent results seen in our Korean Phase 3 and U.S. Phase 2 trials also hold true in the massive Chinese market,” a Jetema official stated. “It is significant because we have secured a safety profile that meets global standards in addition to proven efficacy.” The company plans to complete the Biologics License Application (BLA) in China within the first half of this year and expects significant revenue growth starting next year by adding toxin sales to its existing HA filler business.

Jetema is also moving to dominate the U.S. market by redefining the “skin booster” category. In a previous interview with this publication, Jetema Chairman Kim Jae-young noted, “While the U.S. accounts for half of the global aesthetics market, the skin booster segment is virtually uncharted territory. By combining our FDA-approved hyaluronic acid (HA) assets with patented injection devices, we will bypass the 4-5 year approval process and immediately capture the market.”

| | Recent stock price trend of Genome & Company. (Source: KG Zeroin MP DOCTOR) |

|

Genome & Company Secures Realized Profits Through “Royalty Maximization” Strategy Genome & Company also saw its shares rise by 8.70% to 6,120 won as the results of its strategic licensing deals began to materialize. This rally is attributed to the evaluation that its contract with UK-based Ellipses Pharma for the immunotherapy candidate ‘EP0089 (GENA-104)’ has entered a practical profit-generating stage. Genome & Company recently completed the supply of drug substances for clinical trials to Ellipses, securing its first tangible revenue.

“If we had focused solely on the upfront payment, we would have only received around 5 billion won in short-term profit. Instead, we secured above-average royalty and milestone ratios,” said Bae Ji-soo, CEO of Genome & Company. “By having Ellipses take full responsibility for the 30-40 billion won cost of clinical trials, we created an efficient structure that minimizes risk while maximizing rewards upon success.”

Ellipses is currently conducting large-scale Phase 1/2a trials involving 190 patients in the U.S. and the UK. A Genome & Company official commented, “The supply of drug substances signifies more than just revenue; it represents the trust in our partnership. We expect massive milestone profits when the clinical results are disclosed and secondary licensing occurs.”

| | Recent stock price trend of ToolGen. (Source: KG Zeroin MP DOCTOR) |

|

ToolGen Faces Aftershocks of 70-Billion-Won Capital Increase Amid “Patent War” Despite the overall market boom, ToolGen struggled following news of a massive capital increase. Shares of the gene-editing specialist have been reeling for over ten days since the announcement of a 70-billion-won rights offering on the 15th. On the 29th, the stock plummeted 21.28% to close at 48,100 won. Its share price has crashed 61.6% in just ten trading days from its pre-announcement level of 125,400 won on the 14th.

The company explained that the capital increase is a “strategic decision” to defend the global patent rights of its ‘CRISPR-Cas9’ technology. ToolGen is currently embroiled in an interference proceeding with the Broad Institute in the U.S. to determine the original ownership of the technology.

“As the interference proceedings resumed faster than expected, we required preemptive legal and research funding,” a ToolGen official said. “To maintain a superior position in licensing negotiations with global firms, we needed to demonstrate unshakable financial strength.”

However, the market reacted sensitively to the dilution of shareholder value and short-term selling pressure. The expected offering price in the 90,000 won range (at the time of announcement) placed a heavy burden on investors, and the uncertainty leading up to the listing of new shares froze investor sentiment. While ToolGen emphasized that it requested only the minimum necessary funds to reduce the burden on shareholders, investors prioritized immediate cash flow and dilution concerns over long-term technological value.

Hong Soon jae CEO of BioBook analyzed the situation “ToolGen‘s case proves that no matter how unrivaled a biotech’s technology is, its corporate value can fluctuate wildly based on its financing methods and communication with the market. In a market where capital flows toward stocks with positive catalysts, a capital increase can become a fatal weakness.”

![4일 연속 下 면한 코오롱티슈진…펩트론, 시간외 급등 이유는[바이오 맥짚기]](https://image.edaily.co.kr/images/vision/files/NP/S/2026/07/PS26072700192b.jpg)

![넥스트메디의 바이오헬스케어 미국 규제 실무 전략 [바이오스터디]](https://i.ytimg.com/vi/XAVZkzSxZQo/mqdefault.jpg)